Estate Tax vs Inheritance Tax

Estate Tax vs Inheritance Tax

Planning what happens to your money and property after your death is not an easy task. Many people are concerned about taxes that may affect their families in the future. There are two common taxes people often discuss: estate tax and inheritance tax, which some people also refer to as the death tax.

This guide explains everything about taxes, who pays them, how they work, and how you can reduce tax burden through smart planning. Let's get into:

Planning what happens to your money and property after your death is not an easy task. Many people are concerned about taxes that may affect their families in the future. There are two common taxes people often discuss: estate tax and inheritance tax, which some people also refer to as the death tax.

This guide explains everything about taxes, who pays them, how they work, and how you can reduce tax burden through smart planning. Let's get into:

At a Glance

Estate tax is paid by the estate before money or property is given to the family members. On the other hand, inheritance tax is paid by the person who received the inheritance after the death of their loved one.

The interesting part is that not every state charges these taxes, but the US is the only state that charges both estate tax and inheritance tax. There is no need to worry about; with good planning, everyone can reduce or avoid these taxes effortlessly.

What's the Difference Between Estate Tax & Inheritance Tax

Two ways to differentiate between the two days are to understand who pays the tax and how it is calculated. Here's the cheat sheet to help you understand:

Point of Comparison | Estate Tax | Inheritance Tax |

Who is responsible for payment? | The tax is paid directly from the deceased person’s total property and money before anything is handed over to relatives or beneficiaries. | The person who receives the money, home, or other assets pays the tax after the inheritance is transferred to them. |

Where does the tax apply? | This tax can be charged by the federal government and also by some individual states, depending on local laws and estate value. | This tax only exists in certain states and is not collected at the national or federal level. |

What amount is taxed? | The full value of everything owned by the person at the time of death is reviewed to calculate the taxable amount. | Only the share of property or money that each heir personally receives is used to calculate the tax. |

Who is responsible for payment?

The tax is paid directly from the deceased person’s total property and money before anything is handed over to relatives or beneficiaries. The person who receives the money, home, or other assets pays the tax after the inheritance is transferred to them.

Where does the tax apply?

This tax can be charged by the federal government and some individual states, depending on local laws and estate value. This tax only exists in certain states and is not collected at the national or federal level.

What amount is taxed?

The full value of everything owned by the person at the time of death is reviewed to calculate the taxable amount. Only the share of property or money that each heir personally receives is used to calculate the tax.

Who Pays (Estate & Inheritance)

For Inheritance: Each beneficiary needs to pay tax depending on the state rules. It also depends on the relationship to the decrease. For some reason, many family members mean nothing to them.

For Estate: This tax is totally handled by the executor of the estate (tax payment).

Estate Tax & Inheritance Tax Quires

Many people want to know about estate and inheritance in detail. In the guidelines below, I'll cover basic and important questions that most people ask. Let's clarify the confusion:

What is the Death Tax?

Death tax is not an official legal term; it is basically a term that people use to describe the taxes that they pay after someone's death. It actually means that the state tax and the inheritance tax. You may hear this word in the news, financial discussions, or tax conversations. This term is simple and refers to taxes that are connected to someone's assets after they pass away.

Estate Tax vs Death Tax

Is the tax a real and original legal term that tax authorities use? However, the death tax is just a term that people use to describe it. They are often used when talking about inheritance tax and estate tax. So, if someone says death tax in front of you, you quickly need to realize that he must be talking about the state tax and inheritance tax. This thing lies between both; you need to understand it.

What's the Federal Death Tax?

Many people want to know about the federal death tax. There is no official Federal death tax, but the Federal government only charges a federal estate tax. Let me clarify, if you hear about federal tax, it simply means federal estate taxes.

For example, if a person’s total assets exceed the government’s allowed limit, they must pay the tax before anything is passed on to heirs. This tax is a must in every country, but if you move to the federal inheritance tax, then there is no such tax in the United States.

Was the Death Tax Repeal Act Passed?

No, the law to completely remove the tax has not been approved. Lawmakers have discussed it many times, so the conclusion is that the tax still exists. However, tax rules sometimes change, and the exemption amount usually increases over time. It's mandatory to pay these taxes, and they will further increase in the future as laws.

What's Included in Estate Tax?

An estate includes almost everything a person has when they pass away. It includes:

· Homes

· Land

· Bank Accounts

· Vehicles

· Jewellery

· Business Interest Investments

Life insurance benefits. All the above items together form a total estate value.

What is the Estate Tax Exemption Amount?

The estate tax exemption amount is the maximum value that an estate can have before the Federal estate tax becomes payable. If the total worth of a person's property, including savings and investments, is below the limit, then the government doesn't charge any state tax at all.

For the current year, the amount is set at $13.99 million for individuals. That is higher than the previous year's limit of $13.61 million. This limit increases over time and provides families with relief from federal tax pressure.

This exemption amount is totally adjusted over time to match inflation. It also depends on the rising cost of living. As prices increase in the economy, the exemption level usually increases as well. It proves that all estates are working with rules and are not unfair to anyone.

Estate Tax Exemption Amounts by States

Some states charge their own estate tax. These state limits are usually much lower than the federal exemption. It means that even medium-sized estates can be subject to state taxes. As of the current year, a total of 12+ states, including Washington, D.C., collect estate tax.

The interesting thing is that each location sets its own exemption amount and tax structure. To make it more understandable, here is the list arranged in a different sequence:

State / Region | Estate Tax Exemption (2025) |

Oregon | $1,000,000 |

Massachusetts | $2,000,000 |

Washington | $2,193,000 |

Minnesota | $3,000,000 |

Illinois | $4,000,000 |

District of Columbia | $4,873,200 |

Maryland | $5,000,000 |

Vermont | $5,000,000 |

Hawaii | $5,490,000 |

Maine | $7,000,000 |

New York | $7,160,000 |

Rhode Island | $1,802,431 |

Connecticut | $13,990,000 |

Each state also decides how the tax is calculated. Many States use progressive or marginal tax rates. On the other hand, some States apply a flat tax rate.

Interesting fact: Only six States currently impose an inheritance tax, which includes Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania. On the other hand, Maryland is the only state that charges both estate and inheritance taxes.

What's the Estate Federal Tax Rate?

The federal estate tax does not use a fixed percentage in every state. In fact, the tax amount increases as the portion of the estate becomes larger. But the fact is that only the amount up to the exemption limit is taxed, not the full estate value. The lowest tax starts at 18% and the highest rate is up to 40%. Let's see in detail:

Tax Percentage | Portion of Estate Subject to Tax (Above $13.99 Million Limit) |

18% | First $10,000 of taxable value |

20% | $10,001 to $20,000 |

22% | $20,001 to $40,000 |

24% | $40,001 to $60,000 |

26% | $60,001 to $80,000 |

28% | $80,001 to $100,000 |

30% | $100,001 to $150,000 |

32% | $150,001 to $250,000 |

34% | $250,001 to $500,000 |

37% | $500,001 to $750,000 |

39% | $750,001 to $1,000,000 |

40% | Any amount above $1,000,000 |

Estate Tax Examples

Let's have a look at a few examples to understand how state taxes work in real life:

Example 01: Lilly has an estate valued at $15.38 million. The federal exemption in the current year is $13.99 million, so it means that only the amount above that is taxable, which would be $1.39 million. Since it exceeds $1 million, the highest Federal state tax of 40% applies to the portion above the exemption.

The conclusion is that Lilly's estate would have owed about $556,000 to the IRS. This approximate amount is only before her heirs receive assets. Another condition is if Lily were left in a state that charges estate tax, then the state would calculate its tax separately based on its own exemption and rates.

Example 02: Now imagine that Lily's estate is only worth $2 million. In this scenario, if a state is below the federal exemption limit, there is no need to pay federal estate tax. Moreover, some States have much lower exemptions. As current rules, only Oregon and Rhode Island have exemptions below $2 million. The clear answer is if she lives in a certain island or location where they charge even less than $2 million, so she has to pay in those locations.

These examples show why understanding both Federal and state rules is important. Proper planning can help families to avoid these kinds of surprises and even reduce their overall tax burden.

Conditions for Both Estate & Inheritance Tax File Return

Whether you need to file an estate or inheritance tax return, there are several factors that you need to focus on. It includes where you live, where the deceased lives, and whether the estate or inheritance exceeds the exemption limits. Let's understand one by one:

Filling an estate tax return:

You only need to file a Federal or estate tax return if:

· The total value of the state is higher than the federal exemption.

· The decreased-on property that charges its own tax, and then the estate exceeds that state's examination amount.

· And another situation is if the estate is located in a state with its own tax rules, even if the person who passed away did not live there, you have to file.

Filing an inheritance tax:

You need to file if you find anything that's mentioned below:

· If the value of the property you received meets the state’s filing requirement, you have to file.

· Sometimes you inherit property from someone who lived in or owned the property in a state that charges inheritance tax.

· Another basic reason is that if your relationship to the decrease affects whether you owe the tax, then it's high time to file an inheritance tax return.

How Long Do I Have to File an Estate Tax Return?

Basically, for the federal government, it usually offers you 9 months after the death to file the IRS form. Sometimes people get stuck in their personal matters and want more time. In this scenario, they can request more time. The extension can be offered for only 6 months more. Every state requirement is different; consider the requirements first to proceed further.

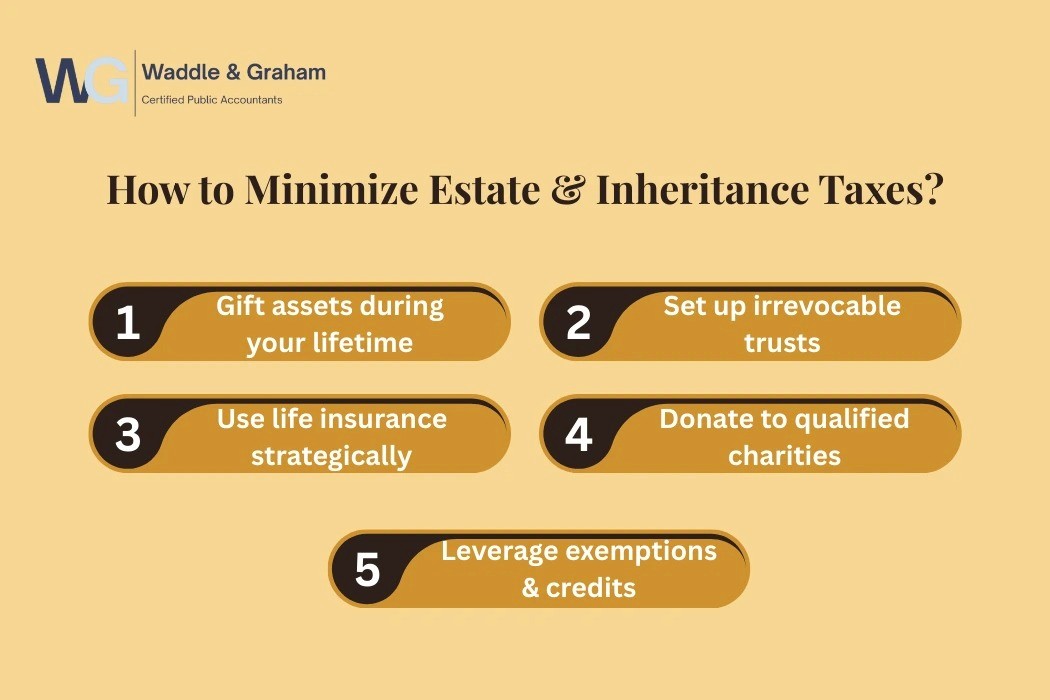

How to Minimize Estate & Inheritance Taxes?

There are several ways to reduce the amount of Texas that your family has to pay. Here are the best suggestions:

One common strategy to gift assets during your lifetime by giving money, property, and all your valuable assets to others can avoid higher taxes later.

Another effective approach to set up an irrevocable trust. In this way, you can shield your property and wealth from estate taxes. Similarly, purchasing life insurance can also provide funds to cover tax bills. This way, your family is not forced to sell property for your investments.

Charity is another strategy that can lower your taxes. You should donate to qualifying charities. It is important to take advantage of state-specific exemptions and tax credits.

From my perspective, these methods are so thoughtful. In this way, you can protect your family's inheritance and reduce the financial burden.

The Bottom Line

Inheritance text and e-state tax sound confusing, but with a basic understanding, you can make your way easier. Correct planning helps you to reduce taxes and even to avoid taxes. Not everyone owes these taxes, because everything depends on proper planning and the rules that apply based on location and estate size. After understanding this guide, you can also take part in protecting your family from these kinds of assets and reduce the future stress of taxes.

FAQs

What's the main difference between estate tax and inheritance tax?

Status paid by the estate, which is before giving to heirs, while inheritance is paid by the person who received the inheritance.

Does every state charge both taxes?

No, only a few states have these taxes. But there is a unique state called Maryland that charges both estate & inheritance taxes.

Are life insurance payouts taxed?

Usually, Life insurance benefits paid to a beneficiary are not taxed. But if the estate owns the policy, then it might count.

Can married couples combine their estate tax exemption?

Yes, each couple can use the unused portion for the surviving spouse. It’s an effective way to double the amount and protect from federal estate taxes.

At a Glance

Estate tax is paid by the estate before money or property is given to the family members. On the other hand, inheritance tax is paid by the person who received the inheritance after the death of their loved one.

The interesting part is that not every state charges these taxes, but the US is the only state that charges both estate tax and inheritance tax. There is no need to worry about; with good planning, everyone can reduce or avoid these taxes effortlessly.

What's the Difference Between Estate Tax & Inheritance Tax

Two ways to differentiate between the two days are to understand who pays the tax and how it is calculated. Here's the cheat sheet to help you understand:

Point of Comparison | Estate Tax | Inheritance Tax |

Who is responsible for payment? | The tax is paid directly from the deceased person’s total property and money before anything is handed over to relatives or beneficiaries. | The person who receives the money, home, or other assets pays the tax after the inheritance is transferred to them. |

Where does the tax apply? | This tax can be charged by the federal government and also by some individual states, depending on local laws and estate value. | This tax only exists in certain states and is not collected at the national or federal level. |

What amount is taxed? | The full value of everything owned by the person at the time of death is reviewed to calculate the taxable amount. | Only the share of property or money that each heir personally receives is used to calculate the tax. |

Who is responsible for payment?

The tax is paid directly from the deceased person’s total property and money before anything is handed over to relatives or beneficiaries. The person who receives the money, home, or other assets pays the tax after the inheritance is transferred to them.

Where does the tax apply?

This tax can be charged by the federal government and some individual states, depending on local laws and estate value. This tax only exists in certain states and is not collected at the national or federal level.

What amount is taxed?

The full value of everything owned by the person at the time of death is reviewed to calculate the taxable amount. Only the share of property or money that each heir personally receives is used to calculate the tax.

Who Pays (Estate & Inheritance)

For Inheritance: Each beneficiary needs to pay tax depending on the state rules. It also depends on the relationship to the decrease. For some reason, many family members mean nothing to them.

For Estate: This tax is totally handled by the executor of the estate (tax payment).

Estate Tax & Inheritance Tax Quires

Many people want to know about estate and inheritance in detail. In the guidelines below, I'll cover basic and important questions that most people ask. Let's clarify the confusion:

What is the Death Tax?

Death tax is not an official legal term; it is basically a term that people use to describe the taxes that they pay after someone's death. It actually means that the state tax and the inheritance tax. You may hear this word in the news, financial discussions, or tax conversations. This term is simple and refers to taxes that are connected to someone's assets after they pass away.

Estate Tax vs Death Tax

Is the tax a real and original legal term that tax authorities use? However, the death tax is just a term that people use to describe it. They are often used when talking about inheritance tax and estate tax. So, if someone says death tax in front of you, you quickly need to realize that he must be talking about the state tax and inheritance tax. This thing lies between both; you need to understand it.

What's the Federal Death Tax?

Many people want to know about the federal death tax. There is no official Federal death tax, but the Federal government only charges a federal estate tax. Let me clarify, if you hear about federal tax, it simply means federal estate taxes.

For example, if a person’s total assets exceed the government’s allowed limit, they must pay the tax before anything is passed on to heirs. This tax is a must in every country, but if you move to the federal inheritance tax, then there is no such tax in the United States.

Was the Death Tax Repeal Act Passed?

No, the law to completely remove the tax has not been approved. Lawmakers have discussed it many times, so the conclusion is that the tax still exists. However, tax rules sometimes change, and the exemption amount usually increases over time. It's mandatory to pay these taxes, and they will further increase in the future as laws.

What's Included in Estate Tax?

An estate includes almost everything a person has when they pass away. It includes:

· Homes

· Land

· Bank Accounts

· Vehicles

· Jewellery

· Business Interest Investments

Life insurance benefits. All the above items together form a total estate value.

What is the Estate Tax Exemption Amount?

The estate tax exemption amount is the maximum value that an estate can have before the Federal estate tax becomes payable. If the total worth of a person's property, including savings and investments, is below the limit, then the government doesn't charge any state tax at all.

For the current year, the amount is set at $13.99 million for individuals. That is higher than the previous year's limit of $13.61 million. This limit increases over time and provides families with relief from federal tax pressure.

This exemption amount is totally adjusted over time to match inflation. It also depends on the rising cost of living. As prices increase in the economy, the exemption level usually increases as well. It proves that all estates are working with rules and are not unfair to anyone.

Estate Tax Exemption Amounts by States

Some states charge their own estate tax. These state limits are usually much lower than the federal exemption. It means that even medium-sized estates can be subject to state taxes. As of the current year, a total of 12+ states, including Washington, D.C., collect estate tax.

The interesting thing is that each location sets its own exemption amount and tax structure. To make it more understandable, here is the list arranged in a different sequence:

State / Region | Estate Tax Exemption (2025) |

Oregon | $1,000,000 |

Massachusetts | $2,000,000 |

Washington | $2,193,000 |

Minnesota | $3,000,000 |

Illinois | $4,000,000 |

District of Columbia | $4,873,200 |

Maryland | $5,000,000 |

Vermont | $5,000,000 |

Hawaii | $5,490,000 |

Maine | $7,000,000 |

New York | $7,160,000 |

Rhode Island | $1,802,431 |

Connecticut | $13,990,000 |

Each state also decides how the tax is calculated. Many States use progressive or marginal tax rates. On the other hand, some States apply a flat tax rate.

Interesting fact: Only six States currently impose an inheritance tax, which includes Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania. On the other hand, Maryland is the only state that charges both estate and inheritance taxes.

What's the Estate Federal Tax Rate?

The federal estate tax does not use a fixed percentage in every state. In fact, the tax amount increases as the portion of the estate becomes larger. But the fact is that only the amount up to the exemption limit is taxed, not the full estate value. The lowest tax starts at 18% and the highest rate is up to 40%. Let's see in detail:

Tax Percentage | Portion of Estate Subject to Tax (Above $13.99 Million Limit) |

18% | First $10,000 of taxable value |

20% | $10,001 to $20,000 |

22% | $20,001 to $40,000 |

24% | $40,001 to $60,000 |

26% | $60,001 to $80,000 |

28% | $80,001 to $100,000 |

30% | $100,001 to $150,000 |

32% | $150,001 to $250,000 |

34% | $250,001 to $500,000 |

37% | $500,001 to $750,000 |

39% | $750,001 to $1,000,000 |

40% | Any amount above $1,000,000 |

Estate Tax Examples

Let's have a look at a few examples to understand how state taxes work in real life:

Example 01: Lilly has an estate valued at $15.38 million. The federal exemption in the current year is $13.99 million, so it means that only the amount above that is taxable, which would be $1.39 million. Since it exceeds $1 million, the highest Federal state tax of 40% applies to the portion above the exemption.

The conclusion is that Lilly's estate would have owed about $556,000 to the IRS. This approximate amount is only before her heirs receive assets. Another condition is if Lily were left in a state that charges estate tax, then the state would calculate its tax separately based on its own exemption and rates.

Example 02: Now imagine that Lily's estate is only worth $2 million. In this scenario, if a state is below the federal exemption limit, there is no need to pay federal estate tax. Moreover, some States have much lower exemptions. As current rules, only Oregon and Rhode Island have exemptions below $2 million. The clear answer is if she lives in a certain island or location where they charge even less than $2 million, so she has to pay in those locations.

These examples show why understanding both Federal and state rules is important. Proper planning can help families to avoid these kinds of surprises and even reduce their overall tax burden.

Conditions for Both Estate & Inheritance Tax File Return

Whether you need to file an estate or inheritance tax return, there are several factors that you need to focus on. It includes where you live, where the deceased lives, and whether the estate or inheritance exceeds the exemption limits. Let's understand one by one:

Filling an estate tax return:

You only need to file a Federal or estate tax return if:

· The total value of the state is higher than the federal exemption.

· The decreased-on property that charges its own tax, and then the estate exceeds that state's examination amount.

· And another situation is if the estate is located in a state with its own tax rules, even if the person who passed away did not live there, you have to file.

Filing an inheritance tax:

You need to file if you find anything that's mentioned below:

· If the value of the property you received meets the state’s filing requirement, you have to file.

· Sometimes you inherit property from someone who lived in or owned the property in a state that charges inheritance tax.

· Another basic reason is that if your relationship to the decrease affects whether you owe the tax, then it's high time to file an inheritance tax return.

How Long Do I Have to File an Estate Tax Return?

Basically, for the federal government, it usually offers you 9 months after the death to file the IRS form. Sometimes people get stuck in their personal matters and want more time. In this scenario, they can request more time. The extension can be offered for only 6 months more. Every state requirement is different; consider the requirements first to proceed further.

How to Minimize Estate & Inheritance Taxes?

There are several ways to reduce the amount of Texas that your family has to pay. Here are the best suggestions:

One common strategy to gift assets during your lifetime by giving money, property, and all your valuable assets to others can avoid higher taxes later.

Another effective approach to set up an irrevocable trust. In this way, you can shield your property and wealth from estate taxes. Similarly, purchasing life insurance can also provide funds to cover tax bills. This way, your family is not forced to sell property for your investments.

Charity is another strategy that can lower your taxes. You should donate to qualifying charities. It is important to take advantage of state-specific exemptions and tax credits.

From my perspective, these methods are so thoughtful. In this way, you can protect your family's inheritance and reduce the financial burden.

The Bottom Line

Inheritance text and e-state tax sound confusing, but with a basic understanding, you can make your way easier. Correct planning helps you to reduce taxes and even to avoid taxes. Not everyone owes these taxes, because everything depends on proper planning and the rules that apply based on location and estate size. After understanding this guide, you can also take part in protecting your family from these kinds of assets and reduce the future stress of taxes.

FAQs

What's the main difference between estate tax and inheritance tax?

Status paid by the estate, which is before giving to heirs, while inheritance is paid by the person who received the inheritance.

Does every state charge both taxes?

No, only a few states have these taxes. But there is a unique state called Maryland that charges both estate & inheritance taxes.

Are life insurance payouts taxed?

Usually, Life insurance benefits paid to a beneficiary are not taxed. But if the estate owns the policy, then it might count.

Can married couples combine their estate tax exemption?

Yes, each couple can use the unused portion for the surviving spouse. It’s an effective way to double the amount and protect from federal estate taxes.

Category

Tax

Date

Feb 10, 2026