A Comprehensive Business Succession Planning Guide

A Comprehensive Business Succession Planning Guide

Planning a business is a remarkable achievement, but one must think about the future. Future ideas about retirement, starting a new company, unexpected situations, leaving a business, all these things matter and can even put the business owner in dangerous situations if he does not plan.

The goal of business succession planning is to leave your company in a successful position. A strong succession plan will assist you in the company’s legacy, value, workforce, and reputation. The true definition of corporate succession planning, its benefits, disadvantages, and different options will be covered in this article. Let’s explore it:

Planning a business is a remarkable achievement, but one must think about the future. Future ideas about retirement, starting a new company, unexpected situations, leaving a business, all these things matter and can even put the business owner in dangerous situations if he does not plan.

The goal of business succession planning is to leave your company in a successful position. A strong succession plan will assist you in the company’s legacy, value, workforce, and reputation. The true definition of corporate succession planning, its benefits, disadvantages, and different options will be covered in this article. Let’s explore it:

What is Business Succession Planning?

The preparation for a change in ownership and leadership of a company is now known as business succession planning. It involved deciding who will actually take over, how this will be completed, and what steps should be taken to guarantee that business as usual will continue further.

A succession plan is important because it reduces confusion and protects the business from risks like:

Sudden retirement or change of ownership

Loss of clients or suppliers during the shift

Legal or tax complications

Decreased employee satisfaction or retention

In addition, succession planning is not only about family-based businesses, but also affects partnerships, large organizations, investors, and small businesses. If a succession planning strategy isn't in place, the company may lose value or possibly fail. A well-thought-out succession plan usually covers:

The process of identifying the potential competitors

It also defines the roles and responsibilities of all members of the company/business

The planning strategy includes planning for taxes and legal requirements

It also ensured the timeline setting for transactions

One of the most important thing planning is how to communicate with the stakeholders is involved

Key Business Succession Planning Options

There is no one-size-fits-all solution for succession planning. The right option depends on the type of business, the owner’s goals, and the available successors. Here are the main options to consider:

1. Passing the Business to a Family Member

To maintain the legacy of the affordable way is to transfer the family-owned business to the next generation. It's a very emotional and satisfying option for the business owners who want to keep the business in the family. Here’s the list of a few advantages and challenges people face in family business:

Advantages:

It maintains the family control and legacy of the business.

One more benefit is that everyone has familiarity with the business culture and values

It allows the business owner to make transactions easily for employees and customers.

Challenges:

Children or family members may not agree to take over the business

One of the biggest challenges is that they may lack the experience or qualification that is not enough to run a business seat

The generational gap can create conflicts and differences between employees

Tax implications can be the biggest challenge because they include inheritance tax or changes in the reliefs. This matter needs to be carefully handled.

Practical Tips:

Always prepare the family members well in advance

Provide proper training sessions that briefly explain mentorship and professional development

Communicate openly with all, discuss expectations and responsibilities with family members

Consider external advisors like accountants and lawyers, who can help to plan taxes and legal transfers

Passing a business to family can be rewarding, but it's important to assess whether all the family members are capable and whether it continue or not

2. Trade Sale

A trade sale involves selling the business to another company, but usually in the same industry. This option allows the owners to make a clean exit from their business and can even generate the highest sale price. There are a few benefits and challenges that people face while using this method. Here's the detail:

Advantages:

The first benefit is that the owners can fully disengage from the business and can invest their time in other tasks

Another advantage is that they can potentially achieve a higher sales price compared to the other options

The involvement and responsibilities are reduced, and the business owner can get their personal space

Challenges:

The new owners may change the company’s direction or affect the employees and customers

Sale negotiations can be long and complex due to diligence and warranties

Tax dealing can be more challenging, especially the capital gains tax

Practical Tips:

Go with a professional valuation that alerts you about the business's worth

Must ensure to prepare the documentation that includes financial statements, contracts, and operational details

Consider how the staff will be affected and communicate with them clearly about their work

It's important to consider the timing because market conditions can affect the sale prices

Trade sales are suitable for business owners who want a clean exit and are less concerned about keeping the business culture intact.

3. Management Buyout (MBO)

Management buyout is a process where the current management team purchases the business. This option keeps the business in familiar hands and ensures that it'll continue better than others. This step is also beneficial to make the transactions smooth. Let's check what challenges they can face:

Advantages:

The buyers already know the business well because they are already part of the company, which means that they can run it smoothly.

They understand the company culture and even help to protect the employees from certain unplanned situations.

In this method, there is less need to find investors from outside.

Challenges:

The selling price may be lower than the selling price to an external buyer. It's the biggest challenge that people face.

The owner may not receive the full payment immediately. They might need to stay involved for some time to let the partners understand the business well.

The payments often depend on future business profits, which can be risky if earnings decrease.

Practical Tips:

Check if the management team is skilled, reliable, and truly committed. It's important to run the business in the long term.

Plan the deals carefully, such as a lying the payments over time or linking some payments to business performance. You need to be conscious all the time.

Talk openly with the employees so they can feel secure and motivated during the business change.

Get help from legal and financial experts. It makes you feel that the sale is safe and well-structured.

MBOs work well for the business if the management team is experienced, capable, and willing to invest in the company's future.

4. Employee Ownership Trust (EOT)

An employee ownership trust (EOT) is a system where employees own the company together through a trust. The business owner sells the company to this trust, and the trust holds the shares for the benefit of all the employees. Let's understand how it's beneficial and what challenges in this journey business owners face:

Advantages:

Employees feel more connected to the business and even work with higher motivation.

It has to create a positive work environment and attract new employees because of the peaceful area.

The seller may receive tax benefits under certain conditions

Challenges:

The owner receives payments over time, and the overall sale price may be lower than expected.

Employee ownership works best only when all teammates cooperate. It can be difficult to share the responsibility with teamwork.

Careful financial planning is always needed to ensure the business has enough money to operate.

Practical Tips:

Make sure the employees are trading and comfortable with shared ownership. If someone has an issue with their responsibility, then change it.

Help them to understand what ownership actually means. Tell them the duties and rewards clearly.

Estimate future cash flow to manage delayed payments, and always plan before executing any step.

Lawyers and tax advisors can set up the trust correctly, so ask for help from them.

Employee ownership is becoming more popular, especially in businesses that care about community and employees. It motivates the employees to work hard because their success is directly linked to the success of the company.

Things to Consider

There are multiple things that need to consider and succession planning guide. Let's get into:

1. Tax Considerations in Business Succession Planning

Tax planning is a very important part of succession planning. There are different ways of transferring a business that can result in different tax costs. These taxes can affect how much money the owner finally receives and when they receive it.

2. Capital Gains Tax

When the business is sold, the owner has to pay capital gain tax. The capital gains depend on the profit he made from selling the shares. In some countries, Business Asset Disposal Relief (BADR) is also available, which reduces the tax rate under certain conditions. That's why good planning helps to take advantage of these releases to lower the tax costs.

3. Inheritance and Estate Planning

In a family business, inheritance tax applies when the ownership is passed on to the next generation. On the other hand, proper estate planning can reduce the tax. It helps to ensure that the family keeps as much value from the business as possible.

4. Deferred Payments

Some succession options, such as management buy-outs or employee ownership trust involve receiving payment over time. This can reduce immediate tax pressure, but it also requires careful planning to manage. This process ensures that the full amount must eventually be received.

Steps to Develop a Business Succession Plan

Creating a succession plan required careful thought and well-planned, structured steps. Here’s a practical roadmap that assists you in building a succession plan for your business:

1. Define Your Goals

Deciding what you want is the main goal. In the planning, you can include family legacy, financial gain, employee ownership, and smooth transactions. You need to plan your goal, taking care of every aspect of the business.

2. Identify Successors

To identify which person of your family is capable for suitable role, look for all members and decide which one is best suited for management employees or external buyers. To make it clear, check their capabilities, skills, experience, and interests.

3. Create a Timeline

Planning the timeline plays an important role in business. Plan the transactions to avoid facing delayed issues. Typical timeline is 3 to 5 years before the plan's exit. The extended timeframe provides enough opportunity to identify and train the successors. It improves the business performance and even resolves the financial or legal issues.

4. Provide Training and Mentorship

Once the potential successors are identified, they must be prepared for the leadership role. This step involves structured training in both technical and managerial areas of the business. The successor should rotate the key departments like finance, operations, sales, and human resources.

Mentorship from the current owner is critical to understand. Regular coaching sessions help more to transfer skills, institutional knowledge, decision-making logic, and company culture.

5. Plan for Taxes and Legal Matters

The major financial and legal implications must be included in the planning. Accountants can help to structure the ownership transfer efficiently. It can be possible through gifts, installments, sales, trusts, and share buy-back arrangements. Lawyers also play an essential role in legal documents (shareholder agreements & partnership contracts) planning.

6. Communicate with Stakeholders

Transparent communication is key to maintaining trust during a leadership transition. Planning meetings with the stakeholders is very important. Always inform the employees, clients, suppliers, and partners about all the transactions to maintain trust and confidence. Introducing the successor and explaining their roles helps to maintain strong relationships and business continuity.

7. Document the Plan

After completing the above steps, now plan the document to avoid confusion. In the document, clearly outline who will take over the leadership, ownership, and management responsibilities. Also mention timelines, performance, benchmarks, and decision-making authority.

8. Review Regularly

Business conditions, market trends, tax laws, and personal goals change over time. It's not even a time activity, so the plan should be reviewed regularly. It must be continued every one to two years to ensure everything is practical. Regular reviews ensured the plan aligned with the company’s long-term strategy. To keep the succession plan updated, always ensure the business remains prepared for both planned and unexpected transactions.

Common Mistakes to Avoid

Common mistakes people usually make in business planning are mentioned below: Let's have a look at them to avoid:

If you want to leave the business, then plan it several years before leaving it. Late planning can reduce the choices and even create pressure.

If someone is not prepared for the specific role in the family, the result issue. Family disagreements can seriously damage the succession process.

Plan the tax details because these matter the most, but don't avoid business culture, leadership, and daily operations.

Clear communication and reassurance are important. Never let your employees and clients be in confusion or disruption.

Avoid all these mistakes to build a smooth transition and protect the future of the business.

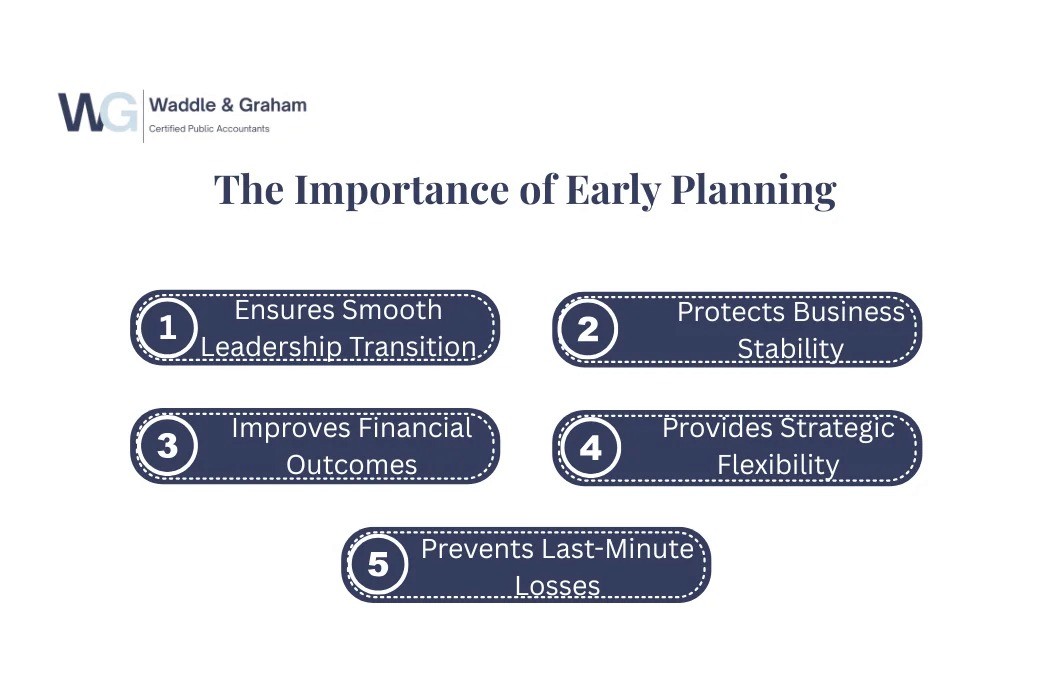

The Importance of Early Planning

Early planning is important because it protects both employees and the business. Starting the business planning process allows a smooth and continuous transfer of knowledge, skills, and responsibilities. This helps to avoid confusion when leadership changes.

It also gives business owners enough time to prepare financially. With proper session planning the owner can reduce tax costs, improve the company's value, and even maximize overall profits. It allows the owner to manage the time to choose the most suitable plan for the business.

Many entrepreneurs delay succession planning until it's too late for them. This often limits their choices and even reduces the value they can receive from the business. Early planning provides flexibility, stability, and a stronger future for the company.

Final Thoughts

Business succession planning is important for the business to exit smoothly. To protect your staff, yourself, and your company’s history, choose the best succession plan. Always get the advice you need as soon as possible. Work with the team to create a successful plan according to the requirements and business needs.

FAQs

1. What is business succession planning?

Business succession planning is the process of deciding who will take over the business in the future and how the ownership and leadership will be transferred smoothly.

2. When should succession planning start?

Succession planning should start as early as possible, ideally three to five years before leaving the business, to avoid stress and rushed decisions.

3. Is succession planning only for family businesses?

No, succession planning is important for all types of businesses, including partnerships, small companies, and large organizations.

4. Can a business owner stay involved after succession?

Yes, some succession options allow the owner to stay involved for a limited time to guide the new leadership and ensure a smooth transition.

5. Why is communication important in succession planning?

Clear communication helps employees, clients, and partners feel secure and prevents confusion during the leadership or ownership change.

What is Business Succession Planning?

The preparation for a change in ownership and leadership of a company is now known as business succession planning. It involved deciding who will actually take over, how this will be completed, and what steps should be taken to guarantee that business as usual will continue further.

A succession plan is important because it reduces confusion and protects the business from risks like:

Sudden retirement or change of ownership

Loss of clients or suppliers during the shift

Legal or tax complications

Decreased employee satisfaction or retention

In addition, succession planning is not only about family-based businesses, but also affects partnerships, large organizations, investors, and small businesses. If a succession planning strategy isn't in place, the company may lose value or possibly fail. A well-thought-out succession plan usually covers:

The process of identifying the potential competitors

It also defines the roles and responsibilities of all members of the company/business

The planning strategy includes planning for taxes and legal requirements

It also ensured the timeline setting for transactions

One of the most important thing planning is how to communicate with the stakeholders is involved

Key Business Succession Planning Options

There is no one-size-fits-all solution for succession planning. The right option depends on the type of business, the owner’s goals, and the available successors. Here are the main options to consider:

1. Passing the Business to a Family Member

To maintain the legacy of the affordable way is to transfer the family-owned business to the next generation. It's a very emotional and satisfying option for the business owners who want to keep the business in the family. Here’s the list of a few advantages and challenges people face in family business:

Advantages:

It maintains the family control and legacy of the business.

One more benefit is that everyone has familiarity with the business culture and values

It allows the business owner to make transactions easily for employees and customers.

Challenges:

Children or family members may not agree to take over the business

One of the biggest challenges is that they may lack the experience or qualification that is not enough to run a business seat

The generational gap can create conflicts and differences between employees

Tax implications can be the biggest challenge because they include inheritance tax or changes in the reliefs. This matter needs to be carefully handled.

Practical Tips:

Always prepare the family members well in advance

Provide proper training sessions that briefly explain mentorship and professional development

Communicate openly with all, discuss expectations and responsibilities with family members

Consider external advisors like accountants and lawyers, who can help to plan taxes and legal transfers

Passing a business to family can be rewarding, but it's important to assess whether all the family members are capable and whether it continue or not

2. Trade Sale

A trade sale involves selling the business to another company, but usually in the same industry. This option allows the owners to make a clean exit from their business and can even generate the highest sale price. There are a few benefits and challenges that people face while using this method. Here's the detail:

Advantages:

The first benefit is that the owners can fully disengage from the business and can invest their time in other tasks

Another advantage is that they can potentially achieve a higher sales price compared to the other options

The involvement and responsibilities are reduced, and the business owner can get their personal space

Challenges:

The new owners may change the company’s direction or affect the employees and customers

Sale negotiations can be long and complex due to diligence and warranties

Tax dealing can be more challenging, especially the capital gains tax

Practical Tips:

Go with a professional valuation that alerts you about the business's worth

Must ensure to prepare the documentation that includes financial statements, contracts, and operational details

Consider how the staff will be affected and communicate with them clearly about their work

It's important to consider the timing because market conditions can affect the sale prices

Trade sales are suitable for business owners who want a clean exit and are less concerned about keeping the business culture intact.

3. Management Buyout (MBO)

Management buyout is a process where the current management team purchases the business. This option keeps the business in familiar hands and ensures that it'll continue better than others. This step is also beneficial to make the transactions smooth. Let's check what challenges they can face:

Advantages:

The buyers already know the business well because they are already part of the company, which means that they can run it smoothly.

They understand the company culture and even help to protect the employees from certain unplanned situations.

In this method, there is less need to find investors from outside.

Challenges:

The selling price may be lower than the selling price to an external buyer. It's the biggest challenge that people face.

The owner may not receive the full payment immediately. They might need to stay involved for some time to let the partners understand the business well.

The payments often depend on future business profits, which can be risky if earnings decrease.

Practical Tips:

Check if the management team is skilled, reliable, and truly committed. It's important to run the business in the long term.

Plan the deals carefully, such as a lying the payments over time or linking some payments to business performance. You need to be conscious all the time.

Talk openly with the employees so they can feel secure and motivated during the business change.

Get help from legal and financial experts. It makes you feel that the sale is safe and well-structured.

MBOs work well for the business if the management team is experienced, capable, and willing to invest in the company's future.

4. Employee Ownership Trust (EOT)

An employee ownership trust (EOT) is a system where employees own the company together through a trust. The business owner sells the company to this trust, and the trust holds the shares for the benefit of all the employees. Let's understand how it's beneficial and what challenges in this journey business owners face:

Advantages:

Employees feel more connected to the business and even work with higher motivation.

It has to create a positive work environment and attract new employees because of the peaceful area.

The seller may receive tax benefits under certain conditions

Challenges:

The owner receives payments over time, and the overall sale price may be lower than expected.

Employee ownership works best only when all teammates cooperate. It can be difficult to share the responsibility with teamwork.

Careful financial planning is always needed to ensure the business has enough money to operate.

Practical Tips:

Make sure the employees are trading and comfortable with shared ownership. If someone has an issue with their responsibility, then change it.

Help them to understand what ownership actually means. Tell them the duties and rewards clearly.

Estimate future cash flow to manage delayed payments, and always plan before executing any step.

Lawyers and tax advisors can set up the trust correctly, so ask for help from them.

Employee ownership is becoming more popular, especially in businesses that care about community and employees. It motivates the employees to work hard because their success is directly linked to the success of the company.

Things to Consider

There are multiple things that need to consider and succession planning guide. Let's get into:

1. Tax Considerations in Business Succession Planning

Tax planning is a very important part of succession planning. There are different ways of transferring a business that can result in different tax costs. These taxes can affect how much money the owner finally receives and when they receive it.

2. Capital Gains Tax

When the business is sold, the owner has to pay capital gain tax. The capital gains depend on the profit he made from selling the shares. In some countries, Business Asset Disposal Relief (BADR) is also available, which reduces the tax rate under certain conditions. That's why good planning helps to take advantage of these releases to lower the tax costs.

3. Inheritance and Estate Planning

In a family business, inheritance tax applies when the ownership is passed on to the next generation. On the other hand, proper estate planning can reduce the tax. It helps to ensure that the family keeps as much value from the business as possible.

4. Deferred Payments

Some succession options, such as management buy-outs or employee ownership trust involve receiving payment over time. This can reduce immediate tax pressure, but it also requires careful planning to manage. This process ensures that the full amount must eventually be received.

Steps to Develop a Business Succession Plan

Creating a succession plan required careful thought and well-planned, structured steps. Here’s a practical roadmap that assists you in building a succession plan for your business:

1. Define Your Goals

Deciding what you want is the main goal. In the planning, you can include family legacy, financial gain, employee ownership, and smooth transactions. You need to plan your goal, taking care of every aspect of the business.

2. Identify Successors

To identify which person of your family is capable for suitable role, look for all members and decide which one is best suited for management employees or external buyers. To make it clear, check their capabilities, skills, experience, and interests.

3. Create a Timeline

Planning the timeline plays an important role in business. Plan the transactions to avoid facing delayed issues. Typical timeline is 3 to 5 years before the plan's exit. The extended timeframe provides enough opportunity to identify and train the successors. It improves the business performance and even resolves the financial or legal issues.

4. Provide Training and Mentorship

Once the potential successors are identified, they must be prepared for the leadership role. This step involves structured training in both technical and managerial areas of the business. The successor should rotate the key departments like finance, operations, sales, and human resources.

Mentorship from the current owner is critical to understand. Regular coaching sessions help more to transfer skills, institutional knowledge, decision-making logic, and company culture.

5. Plan for Taxes and Legal Matters

The major financial and legal implications must be included in the planning. Accountants can help to structure the ownership transfer efficiently. It can be possible through gifts, installments, sales, trusts, and share buy-back arrangements. Lawyers also play an essential role in legal documents (shareholder agreements & partnership contracts) planning.

6. Communicate with Stakeholders

Transparent communication is key to maintaining trust during a leadership transition. Planning meetings with the stakeholders is very important. Always inform the employees, clients, suppliers, and partners about all the transactions to maintain trust and confidence. Introducing the successor and explaining their roles helps to maintain strong relationships and business continuity.

7. Document the Plan

After completing the above steps, now plan the document to avoid confusion. In the document, clearly outline who will take over the leadership, ownership, and management responsibilities. Also mention timelines, performance, benchmarks, and decision-making authority.

8. Review Regularly

Business conditions, market trends, tax laws, and personal goals change over time. It's not even a time activity, so the plan should be reviewed regularly. It must be continued every one to two years to ensure everything is practical. Regular reviews ensured the plan aligned with the company’s long-term strategy. To keep the succession plan updated, always ensure the business remains prepared for both planned and unexpected transactions.

Common Mistakes to Avoid

Common mistakes people usually make in business planning are mentioned below: Let's have a look at them to avoid:

If you want to leave the business, then plan it several years before leaving it. Late planning can reduce the choices and even create pressure.

If someone is not prepared for the specific role in the family, the result issue. Family disagreements can seriously damage the succession process.

Plan the tax details because these matter the most, but don't avoid business culture, leadership, and daily operations.

Clear communication and reassurance are important. Never let your employees and clients be in confusion or disruption.

Avoid all these mistakes to build a smooth transition and protect the future of the business.

The Importance of Early Planning

Early planning is important because it protects both employees and the business. Starting the business planning process allows a smooth and continuous transfer of knowledge, skills, and responsibilities. This helps to avoid confusion when leadership changes.

It also gives business owners enough time to prepare financially. With proper session planning the owner can reduce tax costs, improve the company's value, and even maximize overall profits. It allows the owner to manage the time to choose the most suitable plan for the business.

Many entrepreneurs delay succession planning until it's too late for them. This often limits their choices and even reduces the value they can receive from the business. Early planning provides flexibility, stability, and a stronger future for the company.

Final Thoughts

Business succession planning is important for the business to exit smoothly. To protect your staff, yourself, and your company’s history, choose the best succession plan. Always get the advice you need as soon as possible. Work with the team to create a successful plan according to the requirements and business needs.

FAQs

1. What is business succession planning?

Business succession planning is the process of deciding who will take over the business in the future and how the ownership and leadership will be transferred smoothly.

2. When should succession planning start?

Succession planning should start as early as possible, ideally three to five years before leaving the business, to avoid stress and rushed decisions.

3. Is succession planning only for family businesses?

No, succession planning is important for all types of businesses, including partnerships, small companies, and large organizations.

4. Can a business owner stay involved after succession?

Yes, some succession options allow the owner to stay involved for a limited time to guide the new leadership and ensure a smooth transition.

5. Why is communication important in succession planning?

Clear communication helps employees, clients, and partners feel secure and prevents confusion during the leadership or ownership change.

Category

Compliance

Date

Feb 14, 2026